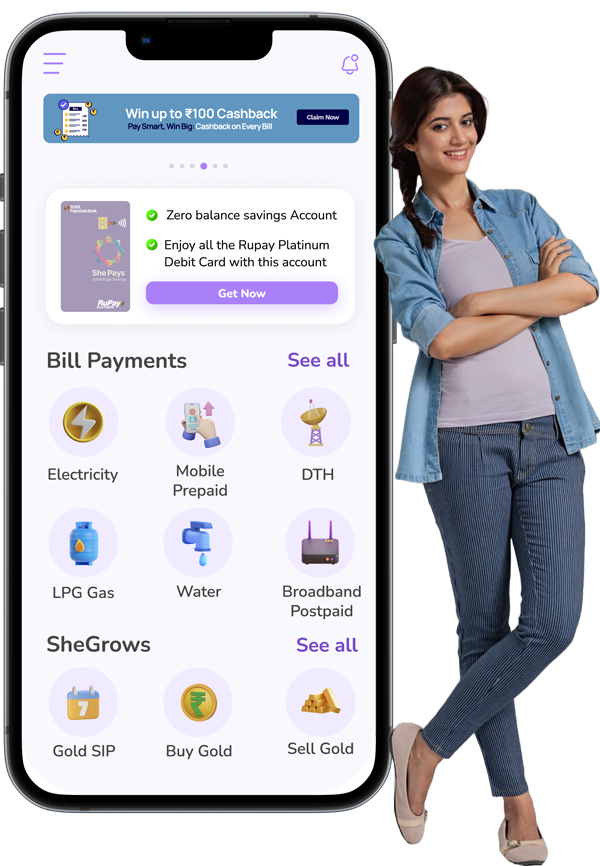

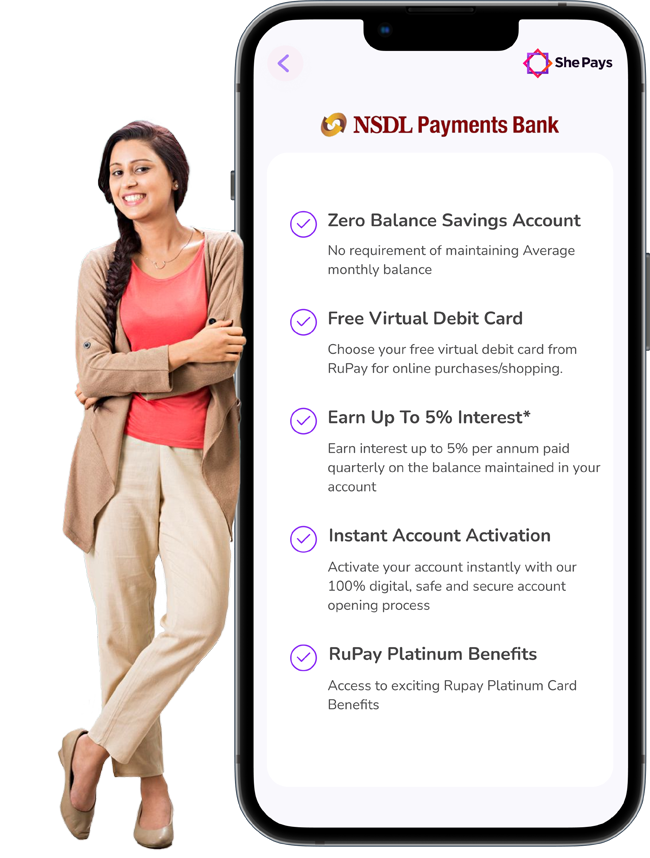

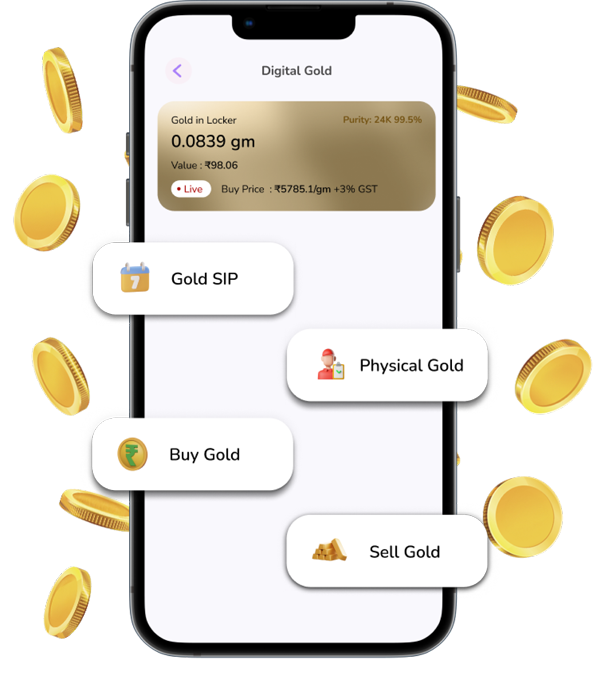

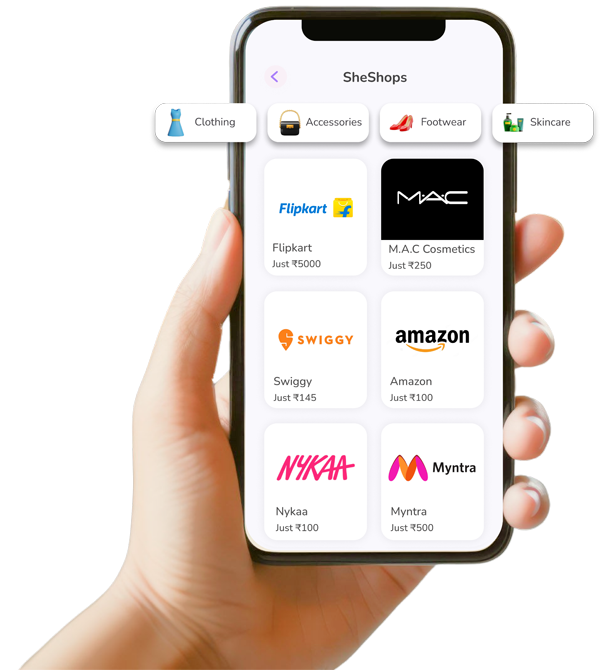

Simplified financial solutions for your future. Get organized, informed, and investing all in one place.